The Australian Government’s First Home Super Saver (FHSS) scheme helps Australians build their first home deposit faster through super contributions. By putting extra money into your super fund, you can take advantage of both tax savings and higher returns, giving you more money to put towards your first home purchase sooner.

What is the First Home Super Saver Scheme?

The FHSS scheme was introduced by the Australian Government in July 2017 to help first-home buyers save for a deposit by using their superannuation.

Under the scheme, you can withdraw up to $50,000 of voluntary contributions made since 1 July 2017, plus associated earnings, to buy or build your first home.

Here’s how it works:

1. Make voluntary contributions

You make extra payments into your super fund. These can be either:

- Concessional (before-tax) contributions such as salary sacrifice.

- Non-concessional (after-tax) contributions paid from your take-home pay.

You can choose to use just one type of contribution or split your voluntary contributions between the two types.

Be aware, however, that standard employer contributions (such as the compulsory Super Guarantee) don’t count and can’t be accessed under the scheme.

2. Build your funds (and save on tax)

You can contribute for as long as you like, but only $15,000 per year and $50,000 in total is eligible under the FHSS scheme.

- Concessional contributions are generally taxed at 15% in your super, instead of your normal income tax rate (which may be 30% or more).

- Non-concessional contributions aren’t taxed when going into your super.

This can make saving for a deposit more tax-effective compared to putting the same money into a regular savings account.

3. Withdraw your FHSS scheme savings

When you’re ready to purchase a property, you must first apply to the Australian Taxation Office (ATO) for an FHSS determination, which tells you the maximum amount you can withdraw. You must apply for a determination before you sign for a property and ownership transfers to you, or you will not be eligible to withdraw FHSS scheme funds.

After receiving a determination, you can apply to release your funds as well as associated earnings on the contributions.

You can request multiple FHSS determinations but can only make one release request.

You must make the release request either before signing a property contract or within 90 days after signing (this was extended from 14 days in September 2024). After requesting a release, you have 12 months to sign a contract to buy or construct your home, which can be extended to 24 months if the ATO approves.

You must also notify the ATO within 28 days of signing your contract. If you exceed this timeframe, a flat 20% FHSS tax applies.

Once approved, the ATO will instruct your super fund to release the money to the ATO, which then transfers the funds to you.

When payment is made, the ATO will tax concessional contributions and earnings at your marginal tax rate with a 30% tax offset. Non-concessional contributions will not be taxed.

Who is eligible for the FHSS scheme?

To participate in the FHSS scheme, you must:

- Be at least 18 years old (though you can make contributions before turning 18).

- Must be purchasing your first property in Australia.

- Have never used the FHSS scheme before.

- Plan to live in the property for at least six of the first 12 months of ownership, or from when the property becomes occupiable.

Note that:

- You don’t need to be an Australian citizen or resident for tax purposes to use the scheme.

- Eligibility is assessed for each buyer separately. This means that if you’re buying jointly, you can still access the scheme even if the other buyer is not eligible. For instance, if you’re a first-home buyer but your partner has owned property before, you may still use the scheme for your share. If both buyers are eligible, each can contribute up to $50,000, giving a combined total of $100,000 towards your first home deposit.

- If you have previously owned property but lost it due to financial hardship (e.g. divorce, natural disaster, bankruptcy, illness or loss of employment), you may still qualify.

How much extra can you save with the FHSS?

The main reason for using the FHSS scheme comes down to tax savings. Let’s look at an example to see how using the scheme could boost your first home deposit.

Say you are earning $90,000 a year, and choose to put $10,000 of that each year towards saving for a home deposit.

- Saving outside of your super in a regular savings account, you would be taxed at your marginal rate of 32% for the 2025–26 tax year (30% plus Medicare levy). You would pay $3,200 in tax on that amount, leaving you with $6,800 saved in one year.

- Saving within your super using the FHSS scheme, you are taxed at just 15%, meaning $1,500 in tax and $8,500 saved in one year.

Here’s how that would accumulate over five years:

| Year | Cumulative contribution | Cumulative net saved outside super | Cumulative net saved with FHSS | Cumulative extra saved |

|---|---|---|---|---|

| 1 | $10,000 | $6,800 | $8,500 | $1,700 |

| 2 | $20,000 | $13,600 | $17,000 | $3,400 |

| 3 | $30,000 | $20,400 | $25,500 | $5,100 |

| 4 | $40,000 | $27,200 | $34,000 | $6,800 |

| 5 | $50,000 | $34,000 | $42,500 | $8,500 |

| Note: This example doesn’t include any interest or associated earnings, either in super or a regular savings account. | ||||

When it comes time to withdraw, your accessible FHSS amount will be taxed at your marginal tax rate but will also benefit from a 30% tax offset.

In this scenario, this is how the numbers would work out:

- 32% tax on $42,500: $13,600

- 30% tax offset: $12,750

- Tax payable: $850

- Amount received: $41,650

Compared to saving outside your super, this would leave you with an extra $7,650 towards your first home deposit.

On top of this, you can also withdraw the earnings on your FHSS scheme contributions. These are calculated using a fixed deemed rate, based on the shortfall interest charge (SIC), which is typically higher than the interest offered on even the best high interest savings accounts.

Why should I use the First Home Super Saver scheme?

If you’re set on trying to get into the property market then the FHSS is a handy scheme to help get you into the property market sooner. Without even factoring in the extra investment return you will get from your super instead of a savings account, you’ll have thousands of dollars more without needing to earn more money.

However, if you’re thinking of wanting a property, but aren’t fully committed to it in the next couple of years then it’s likely best to avoid tying your money up and deal with potential penalties.

Pros and cons of the First Home Super Saver scheme

Pros

-

Save money on taxes

By making voluntary contributions to your super fund under the FHSS scheme, you reduce your taxable income, leaving more money for your home deposit.

-

Build your first home deposit faster

Tax savings and super contributions can help you grow your deposit more efficiently compared to regular savings accounts.

-

Grace period to purchase your home

After withdrawing FHSS funds, you have up to 12 months to buy your first home, extendable to 24 months on request.

-

Fixed, predictable earnings

The SIC rate is generally higher than standard savings account interest and is not impacted by market fluctuations.

Cons

-

Contribution limits

You can only contribute up to $15,000 per year and $50,000 in total under the FHSS scheme, which is unlikely to cover a full deposit.

-

Complex rules

The FHSS scheme can be complex, and you need to follow the process carefully, making sure all requirements are met.

-

Potential penalties

If you miss the deadlines for requesting funds or purchasing your property, you may face FHSS tax penalties.

-

Limited flexibility

If you change your mind about buying a home, your contributions generally must remain in your super until retirement or be withdrawn with additional tax applied.

Can I use the FHSS scheme and 5% Deposit Scheme together?

While the FHSS scheme allows you to save for your home deposit through voluntary super contributions, the 5% Deposit Scheme (formerly the First Home Guarantee) can help you purchase a property with a smaller deposit by acting as a guarantor and reducing or eliminating lenders mortgage insurance (LMI). Both programs can be used when applying for a home loan to make buying your first property easier.

It’s important to note that each program has its own eligibility rules, such as income limits or property requirements, and you’ll need to make sure you meet the conditions for both the FHSS scheme and the 5% Deposit Scheme before applying.

Not sure where to start with your first home? More than 90% of first home buyers plan on using a mortgage broker to get on the property ladder. Talk to a Savvy mortgage broker for free to explore which properties and lenders suit your situation and get expert guidance along the way.

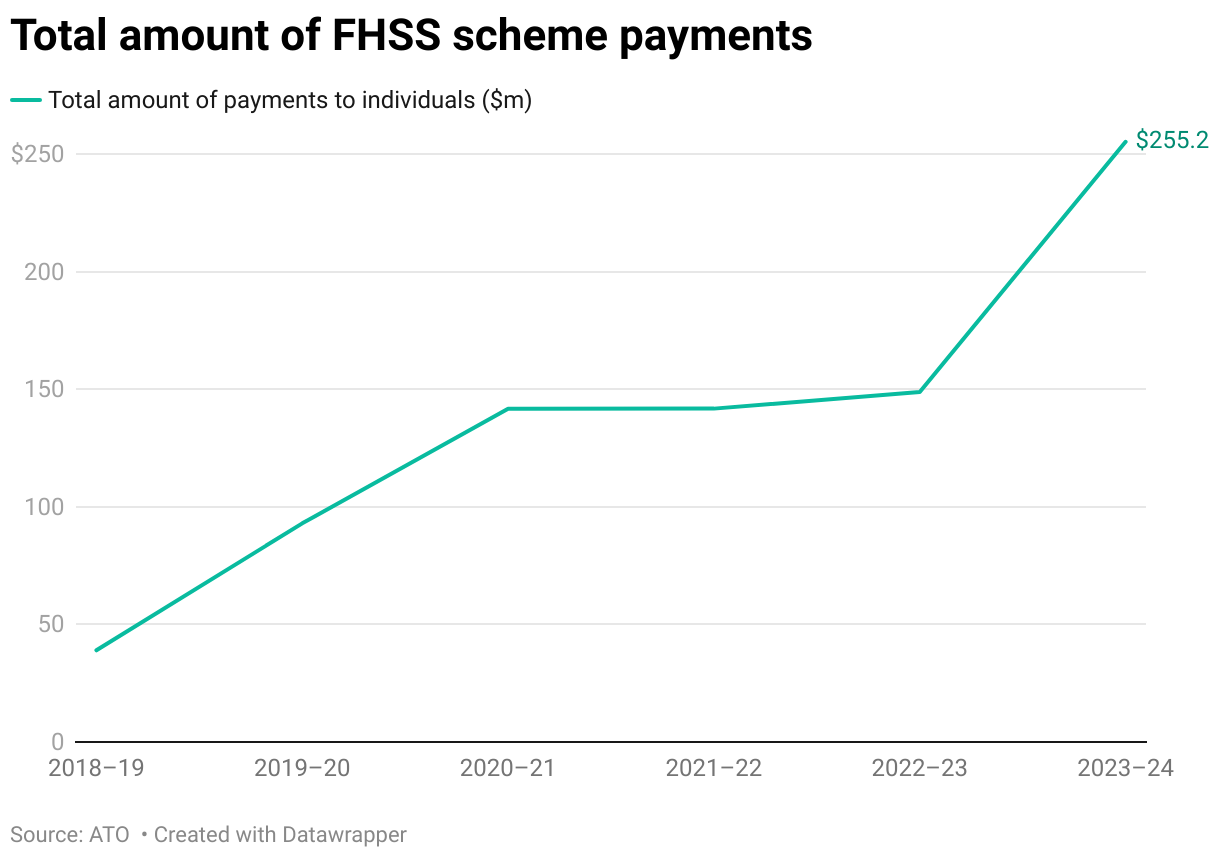

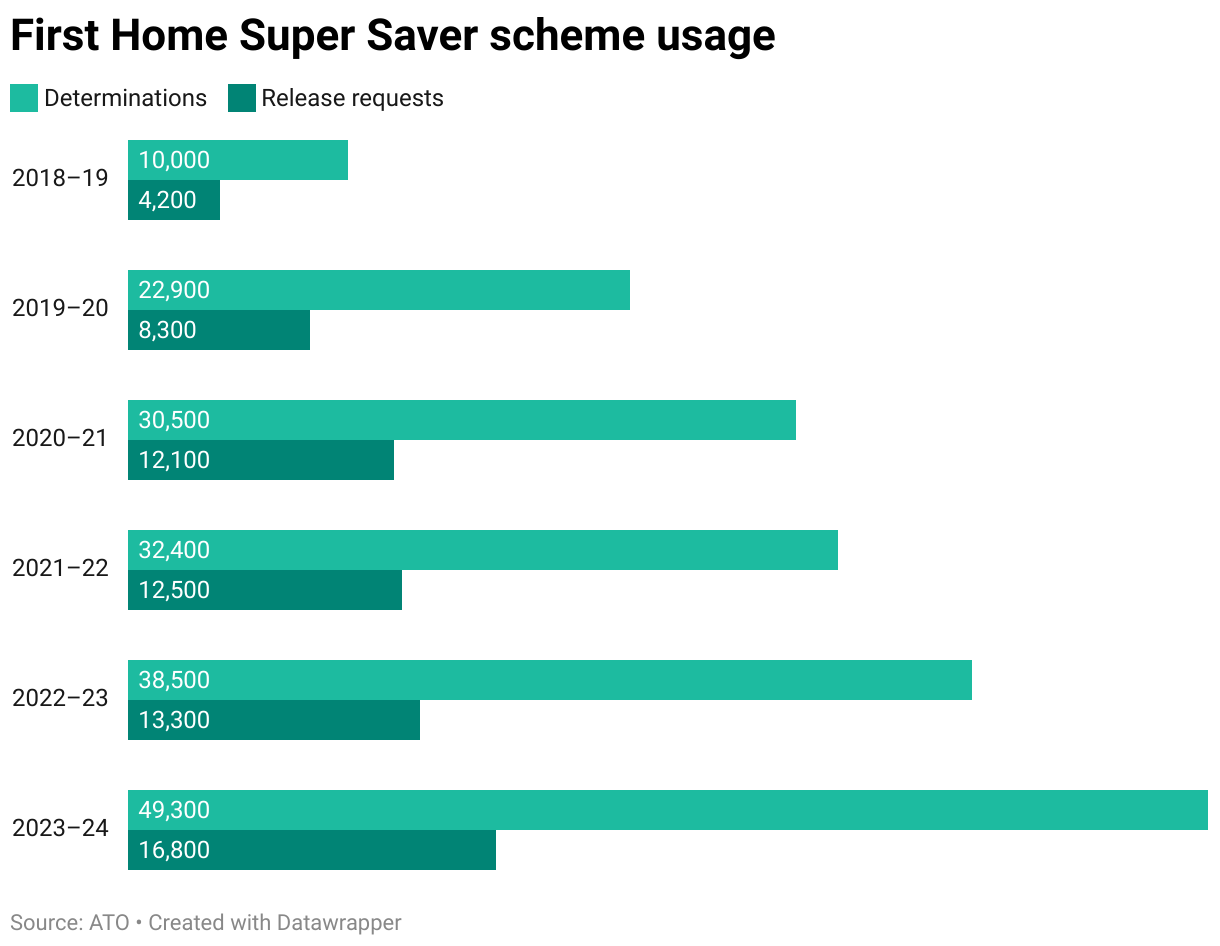

How many people use the First Home Super Saver scheme?

The use of the FHSS scheme has steadily grown since its introduction in 2017. According to ATO statistics, in 2018–19, there were 10,000 determinations and 4,200 release requests. By 2023–24, determinations had risen to 49,300, while release requests reached 16,800 – a near fivefold increase in determinations and a fourfold increase in release requests over six years.

In this time, the total amount of payments to individuals under the scheme increased from $38.9 million in 2018–19 to $255.2 million in 2023–24. After a period of relative stagnation during the Covid years, payments jumped by almost 72% between the 2022–23 and 2023–24 financial years.