12 November marks the deadline for private health insurers to submit their proposed premium changes for 2026 – but not every insurer plays by the rules.

Each year, funds must apply to the Department of Health and Aged Care and APRA to justify any increase, with approvals announced by late January and changes taking effect from 1 April. In 2025, premiums rose by an average of 3.73%, but Australians could face steeper hikes in 2026 as rising hospital costs, higher wages and inflation drive up expenses.

Some insurers have found ways to charge even more – without going through this approval process. Through a practice known as phoenixing, funds can close old products and launch near-identical ones with higher prices, forcing new customers to pay extra for essentially the same cover.

The loophole driving up health insurance prices

Phoenixing has driven up the cost of top-tier private health insurance policies, far exceeding government-approved average increases.

In 2025, for example, HCF closed its Premium Gold policy to new members and replaced it with one that was essentially the same – but 34.6% more expensive.

The increase is even greater in the long term. According to CHOICE, over the past five years, phoenixing has pushed the cost of Gold hospital insurance up by about 58% while the government-approved premium increased by just 16% across all hospital and extras policies.

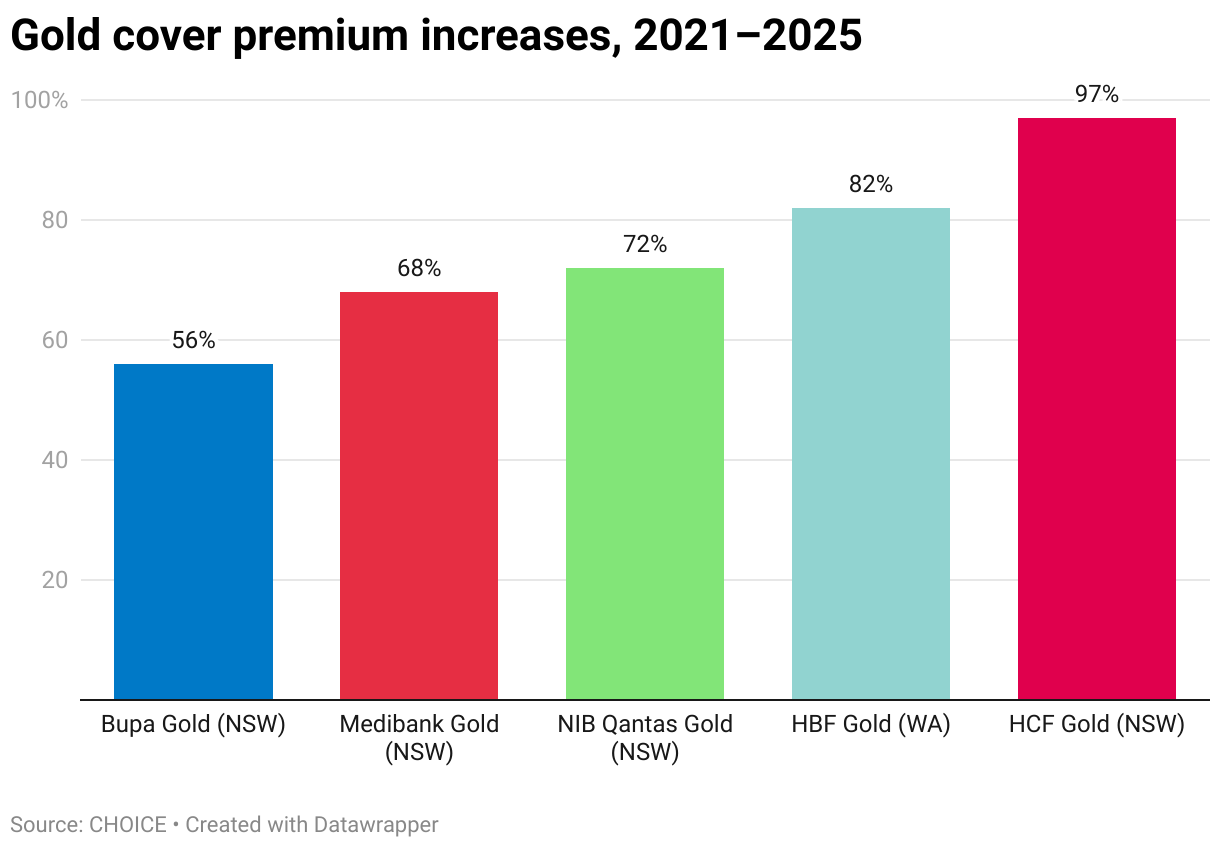

Hospital cover levels

Australia has four hospital cover tiers: Basic, Bronze, Silver and Gold. Gold is the most comprehensive – and costly.

You can also buy extras cover for out-of-hospital services as part of your plan or on its own.

The major health funds have all raised the cost of their Gold-level cover even more than this since January 2021.

Phoenixing in the spotlight

Private health insurers have long used the phoenixing loophole to bypass the government-approved annual review process and raise prices – but it recently hit the headlines after CHOICE published a report highlighting the tactic.

-

February 2024 – CHOICE raises concerns

Consumer group CHOICE published a report highlighting how insurers used phoenixing to increase prices on Gold-level health insurance policies.

-

December 2024 – Commonwealth Ombudsman report

The Commonwealth Ombudsman released a report investigating these loophole tactics, finding that phoenixing undermined regulatory controls designed to protect consumers from unjustified premium hikes.

-

March 2025 – Government investigation

Health Minister Mark Butler called for an urgent investigation into premium increases exploiting regulatory loopholes after calling out insurers for their ‘price-gouging’ tactics.

-

September 2025 – Proposed legislative reform

In response, the government introduced a reform proposal to outlaw phoenixing.

What happens next?

While the exact timing of the legislation is yet to be confirmed, the reforms are expected in time for the 2026 premium round starting on 1 April 2026. Under the new rules, insurers would be required to seek ministerial approval for every new health insurance product, which is the same standard applied to premium increases on existing policies.

The Department of Health has advised insurers to prepare for these changes and, in the meantime, has urged them to stop exploiting this loophole.

What this means for policyholders

Phoenixing means some Australians end up paying more than they need to, especially those on newer or top-tier policies. These steep hikes don’t just increase costs – they also discourage competition.

Many policyholders stay on older, cheaper plans to avoid sudden price jumps, which limits their options and locks them in.

Others might downgrade their cover to save money but risk being underinsured, leaving them exposed if they need treatment not covered by their cheaper policy.

Whether through phoenixing or regular premium increases, rising costs are a good reminder to shop around. Comparing policies can help you find cover better suited to your needs and budget – and switching could save you hundreds each year.

How much does a health insurance plan cost?

The cost of private health insurance varies depending on things like your age, income, where you live and the level of cover you take out.

As an example, here’s what a single 35-year-old living in Sydney could currently expect to pay for their hospital cover:

| Hospital cover tier | Fortnightly cost | Annual cost |

|---|---|---|

| Basic | $39 – $44 | $1,018 – $1,054 |

| Bronze | $45 – $56 | $1,160 – $1,462 |

| Silver | $59 – $98 | $1,542 – $2,443 |

| Gold | $176 – $192 | $4,587 – $4,990 |

| Prices sourced from Compare Club in November 2025 Prices are based on a single 35-year-old on a base tier income living in Sydney (2000) with a $500 excess Note that Gold-level policies checked all include extras Amounts are rounded to the nearest dollar |

||

As you can see, there’s a wide price range even within the same level of cover, and a significant jump between Silver and Gold tiers.

Tips for choosing the right health cover

-

Look at other health funds

Don’t just focus on what your current provider can offer you – compare other insurers to see if there’s a better value plan that still covers what you want.

-

Make sure you’re not overpaying

Regularly review your policy to ensure you’re not paying for extras or services you don’t use. As an example, if your family is complete, then there’s no need to have pregnancy cover anymore.

-

Don’t risk being underinsured

It might be tempting to downgrade your cover to cut costs – but it should still provide the cover you need. Cheap cover isn’t helpful if it doesn’t protect you when you need it most.

-

Explore other tiers

Don’t just focus on one level of cover. Be open to exploring different tiers – some Silver or Silver Plus policies may cover all the services you need without the higher price tag of Gold.