Dealerships are the most common place for Australians to purchase their cars. In the first half of 2025, the Federal Chamber of Automotive Industries (FCAI) reported that 608,811 new cars were delivered, the vast majority of which were purchased through dealerships. Additionally, 529,573 used cars (46.7% of all used car sales) were sold through dealerships, according to the Australian Automotive Dealer Association (AADA).

If you’re ready to walk in, sign your purchase contract and take out a loan with your dealer, though, it’s worth taking a step back and spending more time considering your finance options. Full disclosure: Savvy is a car and asset finance broker, so we help our customers secure loans through our lending partners. However, that doesn’t make it any less important to share valuable tips and insights about what goes into dealer finance compared to a standard car loan.

How is dealer finance different from standard car loans?

Dealer finance is simply the name for the loan your dealership offers you when you buy your car. They function in pretty much the same way as any other regular car loan (secured loan, borrow a lump sum, repay with interest and fees over a set period), but there are a few notable differences:

- Dealer finance is frequently advertised with lower interest rates and framed as a sale (sometimes as low as 1.00% p.a. or even 0% p.a.), though these may only apply to certain makes and models.

- While uncommon on most car loans, dealer finance will often require you to include a balloon payment (lump sum to be paid at the end of the loan).

- In many cases, your dealer won’t offer finance for used cars, instead saving these offers for brand-new models.

- You may not be able to take as long to repay your dealer-financed loan, with caps of three to five years instead of the seven that many lenders offer.

- Your dealer may offer other inclusions, such as extended warranty, free or discounted servicing, fabric protection or window tinting (though you’ll need to consider whether these are worthwhile add-ons).

It’s worth noting that the add-ons in the last point are where dealerships make most of their money, not from the sale of the car itself. For this reason, you may find that sales reps encourage you to add these to your finance package, so be sure to cast a critical eye over how useful they really are.

The pros and cons of dealer finance

Pros

- Applying for finance through your dealer is convenient if you’re already buying your car from them.

- You’ll have your dealer rep on hand to help with your application, who can prepare and submit it for approval.

- You can be approved for a much lower initial interest rate.

Cons

- You’re restricted to vehicles sold by your dealer, often exclusively new models.

- Low interest rates are typically part of an introductory offer and revert to a higher rate after six to 12 months (if the lower rates are available to you at all).

- The lower rates may also result in the purchase price of your car being inflated.

- Although balloon payments reduce your repayments, they also increase your overall interest and make it difficult to sell your car during your loan term.

The pros and cons of car loans

Pros

- You have more power to compare a wider range of options and shop around to see which one suits your needs.

- Provided it fits within your lender’s criteria and your borrowing power, you’ll be able to buy any car, new or used, from a dealership or private seller.

- You won’t be required to add a balloon payment to your loan agreement.

- You’ll have more flexibility when it comes to choosing your loan term.

Cons

- Car loans may take longer to approve than they would through a dealer.

- To commit to finding the best deal, you may have to set a fair amount of time aside to compare options (though this isn’t the case if you engage a broker).

- You can’t approach your lender to make any adjustments to the vehicle or include other add-ons.

How much will my car loan cost vs dealer finance?

Before buying your car, it’s important to understand all the potential costs involved, whether you’re taking out dealer finance or a loan through a bank or another lender. Beyond the loan amount itself, you also need to consider factors such as:

- Vehicle interest rate: the percentage you're charged on the amount borrowed to repay the car loan over time. This includes whether your rate applies across your loan or is only an introductory rate that increases after a set period.

- Comparison rate: the “true” cost of the car loan, including the interest rate and any additional fees like establishment and monthly charges.

- Loan amount: the more you borrow, the more you’ll end up paying in interest overall.

- Repayment period: the total length of time (months or years) you have to repay the car loan in full.

Here is an example of two car loans, one through a dealer and the other through a car loan broker, for a $30,000 car to be paid over a four-year period:

| Dealer finance | Car loan | |

|---|---|---|

|

Interest rate

|

3.00% p.a.

|

6.50% p.a.

|

|

Comparison rate

|

8.00% p.a.

|

7.50% p.a.

|

|

Monthly repayment

|

$733

|

$726

|

|

Total interest and fees

|

$5,155

|

$4,818

|

| Calculations are for illustrative purposes only and actual costs can vary depending on factors like your credit score, lender specifics and dealership promotions. | ||

As you can see, although the dealer offers a lower initial interest rate, the additional fees involved push up the overall cost of the loan, making it more expensive than the car loan found by the broker.

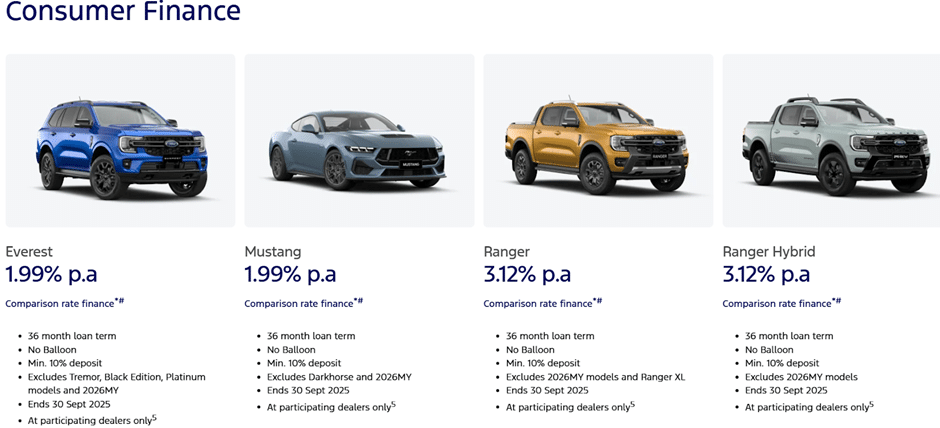

Let’s take a real-world look at how much dealer finance can cost you with a current offer from Ford. You can purchase a Ford Everest and receive a comparison rate of just 1.99% p.a., which looks great at first glance.

Correct as of September 2025.

However, here are the conditions you’ll need to meet:

- You must repay your loan over three years.

- You must pay a minimum deposit of 10%.

- You must buy an approved Everest model, meaning no Tremor, Black Edition, Platinum or MY2026 models.

This means that a 2025 Ford Everest Sport 4WD, which starts at $74,640 before stamp duty and other purchase costs, would require you to pay a deposit of $7,464 and massive monthly instalments of $2,138.

While this would result in a very modest overall interest and fee bill of $2,312, a borrower with the average monthly mortgage payments of $4,055 (according to Canstar) would be forking out almost $6,200 per month and almost $76,500 per year on their house and car alone. For Australians earning the average weekly wage of $2,010 or $104,520 annually, according to the Australian Bureau of Statistics (ABS) as of May 2025, that arrangement simply isn’t feasible.

Common car dealership finance traps

We’ve already spoken about things like low headline rates that aren’t always as they seem, mandatory balloons and term lengths, inflation of your car’s purchase price, limited choice of vehicles and common upsold extras. However, there are a few other things to look out for when it comes to dealer finance:

Guaranteed future value (GFV)

GFV is a common feature of dealer finance. It’s a commitment from your dealership that your car will be worth a certain amount at the end of your term, which is what you’ll pay if you want to keep the car or receive in return if you choose to trade it in.

While knowing what your car will be worth at the end of your term adds a level of certainty, the value your dealership chooses may be lower than what you’d receive by selling your car privately.

What’s also important to note is that GFV is partly based on a kilometre allowance, so exceeding that allowance could reduce that value or leave you paying expensive fees to your dealership.

Trade-ins

A follow-on from the previous point is that dealerships have been known to undervalue vehicles that are traded in as part of your finance deal. That means that you’ll potentially be paying more for your new car and receiving less for your old one. It’s important to weigh up the convenience of a trade-in with the loss in funds compared to selling your car privately.

Taking a deposit before the deal is done

One big one that’s often overlooked is the fact that dealerships will often take a deposit for your car before your finance deal is 100% sorted. Although deposits are refundable under the right circumstances, it may mean going through the rigmarole of getting it back from your dealership if your car loan application isn’t approved.

Adding accessories to the finance

Be it discounted accessories or those sold at standard price, dealerships can push these onto people who will then also have to pay interest on them as part of their package. Aftermarket accessories may be cheaper than having them included in your finance deal, but they’ll catch you on the convenience side.

Vehicle warranty

While some vehicles might come with warranties of up to ten years, it’s often in the terms and conditions that the warranty only stands if the car is serviced at that dealership. Not only does that mean that you’ll have to say goodbye to your preferred mechanic (if you have one), but car dealerships in general are often far more expensive. However, you might feel it’s worth it to have the warranty in place and give yourself peace of mind.

Smaller lending panel

Comparing options on your own means you can consider as many lenders as you like, while the best brokers will have wide and diverse panels of lending partners to choose from. Dealerships, on the other hand, tend to have fewer lenders on their panels. This means your sales rep won’t be scouring the market to secure you the best rate and terms.

How can I get the most out of my car finance deal?

Let’s take a look at a few simple steps you can take to maximise your comfort and savings on your loan deal, all the way through the process:

Before you apply:

- Improve your credit score: a higher credit score qualifies you for lower interest rates, saving you money in the long run.

- Shop around: don't just apply for the first deal you find. Compare rates from a range of lenders to give yourself the best chance of finding a great deal.

- Consider a larger down payment: a bigger deposit reduces your loan amount and monthly payments. It can also improve your chances of getting approved for a loan.

During the application process:

- Understand the loan terms: always read and understand your loan agreement before signing. Doing this helps you avoid any unwanted surprises when it comes to your fees and interest down the track.

- Avoid extras you don't need: think carefully about whether you actually want the add-ons your dealer is trying to sell you. Err on the side of caution and save money if you aren’t sure.

After you’re approved:

- Make payments on time: a consistent payment history helps maintain a good credit score, which can benefit you in the future.

- Consider early repayment: if your loan agreement allows it, paying off your loan ahead of schedule can save you a considerable amount on interest (as long as you don’t have to pay hefty early termination fees).

- Refinance if rates drop: if interest rates drop significantly after you get your loan, consider refinancing to a lower rate (again, provided you won’t be slugged with early termination fees for doing so).

Remember, don't be pressured into a financing deal that doesn't fit your budget or needs. Take your time, do your research and prioritise getting the best possible rate and terms for your car loan.

So, which option is better for me?

The best option for you might be different from the next person. For example, if you want to have everything sorted at the same time and place you buy your car, you’ll probably be leaning towards finance through a dealer. If you want to buy a car from a private seller or avoid a balloon payment, going to a specialist lender will be the better option for you.

What doesn’t change, though, is that the best thing you can do is compare a range of quotes before you settle on your loan. Doing this means you can be more confident that the deal you choose is the most suitable and affordable for your circumstances.

It also pays to ask questions. If you find an offer through a dealer that seems far cheaper than what you’d receive from a bank, be sure to study the terms and conditions of the deal before you sign off on it.