Let’s not beat around the bush: times are tough at the moment. A year ago, we were being told by economists and the media to expect ongoing interest rate cuts. While rates fell in February, May and August 2025, they’ve started to rise again this year.

Throw fuel prices jumping by 30% into the mix, and budgets just aren’t stretching as far as they used to.

While property prices in Australia have jumped by 47% since 2020, for many, that wealth exists on paper, not in their bank account.

Rate reality check

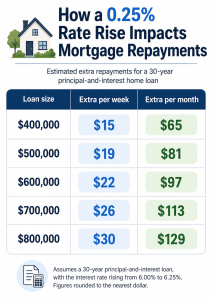

Next week, the RBA meets again, with all Big Four banks predicting another 0.25% increase to the cash rate. That’s roughly another $20 a week out of the hip pockets of families with a $500,000 mortgage.

It’s also worth remembering that every time interest rates go up, your borrowing power goes down. Even if you’ve built up significant equity in your home, any refinance or new loan still comes down to whether you can comfortably afford the repayments.

The risk of mortgage stress

As costs rise and repayments increase, more households are feeling the squeeze.

If you’re struggling to keep up with your home loan, you may be experiencing mortgage stress. This is commonly defined as spending around 30% or more of your income on mortgage repayments.

According to Roy Morgan research, as of April 2026, 26.8% of mortgage holders (around 1.45 million people) are at risk of mortgage stress. This is comparable to levels recorded during the COVID-19 pandemic, according to Savvy's 2021 Housing Affordability Survey. While interest rates were around 3.1% at that time, a higher unemployment rate meant many households were under similar financial pressure.

With another rate rise expected in May, that figure could climb further still, with Roy Morgan predicting the proportion of households at risk of mortgage stress could reach as high as 30.4%.

If your repayments are already feeling stretched, it may be worth reviewing your loan and looking at your refinance options.

Explore your refinancing options

Lenders typically require you to hold at least 20% equity in your property, meaning they’ll lend up to 80% of its value.

For example, if you purchased a $600,000 property with a 20% deposit, your original loan would have been $480,000. If that property is now valued at $950,000, you could have around $470,000 in equity available to borrow against, not including the portion of your loan you’ve already paid off.

However, if you’re already under financial pressure, refinancing your loan back up to 80% of the property’s value may not be realistic. On a $950,000 home, that could mean borrowing up to $760,000, with repayments of approximately $4,557 per month.

In some cases, accessing a smaller amount of equity to pay off higher-interest debt or cover larger expenses, such as replacing a high-cost car with a more efficient vehicle, may help you avoid relying on credit cards to bridge the gap.

Alternatively, you could choose to keep any accessed funds in an offset account, reducing the interest charged on your loan. Just keep in mind that increasing your loan size will generally raise your minimum repayments, even if the funds aren’t spent.

If rates go up next month, is it too late?

No, but if things are feeling tight, it’s worth acting sooner rather than later. With further RBA meetings scheduled in June, August and September, any additional rate rises could add further pressure to household budgets.

“The whole refinancing process typically takes around four to six weeks if you’re changing lenders,” Savvy Home Loans Expert Daniel Carter said.

“Even though the new lender may approve you within a day, the existing lender can take weeks to submit discharge papers.

“If rates go up while you’re refinancing, it’ll be passed onto you in the event you’re applying for a new variable loan.

“Your only way around this is by paying a ‘rate lock’ fee (usually $200 to $500), which means your rate will remain at what it was approved at and usually lasts 90 days.

“Some lenders automatically apply a rate lock at approval without charging a fee, such as Bendigo Bank, so don’t let a rate hike put you off acting on your mortgage.”