Motorbike loan rates

These are the cheapest motorbike loan interest rates available through Savvy as of March 2026:

What is a good interest rate for a bike loan?

As you can see from the table above, the lowest motorcycle loan rate available through Savvy right now is 6.48% p.a. However, the average rate on a motorbike loan approved for a borrower with good credit in the 2025 calendar year was 11.18% p.a.

In reality, the best rate for one person is likely to be different to the next, as it comes down to factors like:

- Your income

- Your employment history

- Your credit score and history

- The size of your loan (for reference, the average motorbike loan approved through Savvy was $17,852 in 2025)

- The age and condition of your bike (the median age of bikes financed through Savvy in 2025 was one year)

- Whether you own your home

What types of motorbikes can you finance?

With Savvy, you’ll be able to buy any of the following motorbikes and finance them with a loan through one of our lenders:

- Adventure/dual-sport bikes

- Cruiser bikes

- Dirt bikes

- Quad bikes/ATVs

- Scooters

- Sport bikes

- Touring bikes

In terms of more recent sales data, 92,967 new motorbikes were registered in 2025, which is a marginal decrease of 1.3% compared to the overall total recorded in 2024. Scooters (+3.8%) were the only segment that saw real growth across the 12 months, with off-road bikes recording 12 more sales than the year prior.

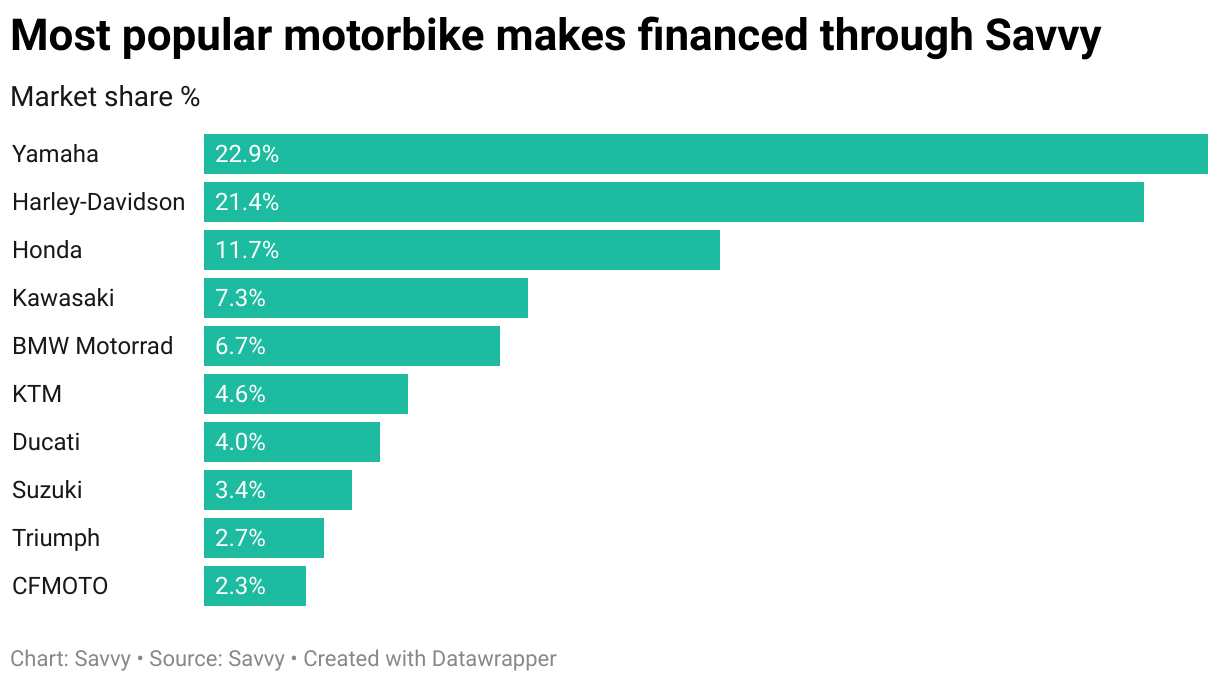

You can see the most popular bikes financed by Savvy customers across 2025 here:

Road bike vs dirt bike finance

Although you can take out a loan to buy any of the above motorbike types, they won’t all be assessed the same way by lenders. One clear example is how road bikes are treated compared to dirt bikes. You’re likely to find that the interest rate on a dirt bike loan is higher than what you’d receive on a regular roadworthy motorbike.

There are several reasons for this, but the most obvious is that the way you use your dirt bike leaves it open to damage and potentially being written off. While standard motorbikes have their risks (more on that in a bit), you won’t be using them to tackle all-terrain obstacle courses or perform tricks. Lowering the value of the bike means your lender could be out of pocket if you become unable to pay off your loan, as they won’t be able to recoup their funds by selling it.

How to finance your dirt bike

"Nearly all dirt bikes require an unsecured loan, as lenders see them more as toys or hobbies than regular vehicles. While this may mean a slightly higher rate, these loans allow you to include all the gear you need, like a helmet, boots and even a trailer."

Why apply for a leisure loan with Savvy?

How to apply for your motorbike loan with Savvy

-

Apply online

Complete our online form and tell us about the bike you want.

-

Supply documents

Send through any documents we need to verify your profile.

-

Talk to your broker

We’ll call you to discuss your motorbike finance options.

-

Have your application prepped

Your broker will put everything together and send it to the lender.

-

Sign on the dotted line

Once it’s approved and settled, all that’s left is to get your bike!

Motorcycle loan calculator

Your estimated repayments

$98.62

| Total interest paid: | Total amount to pay: |

| $1233.43 | $5,143.99 |

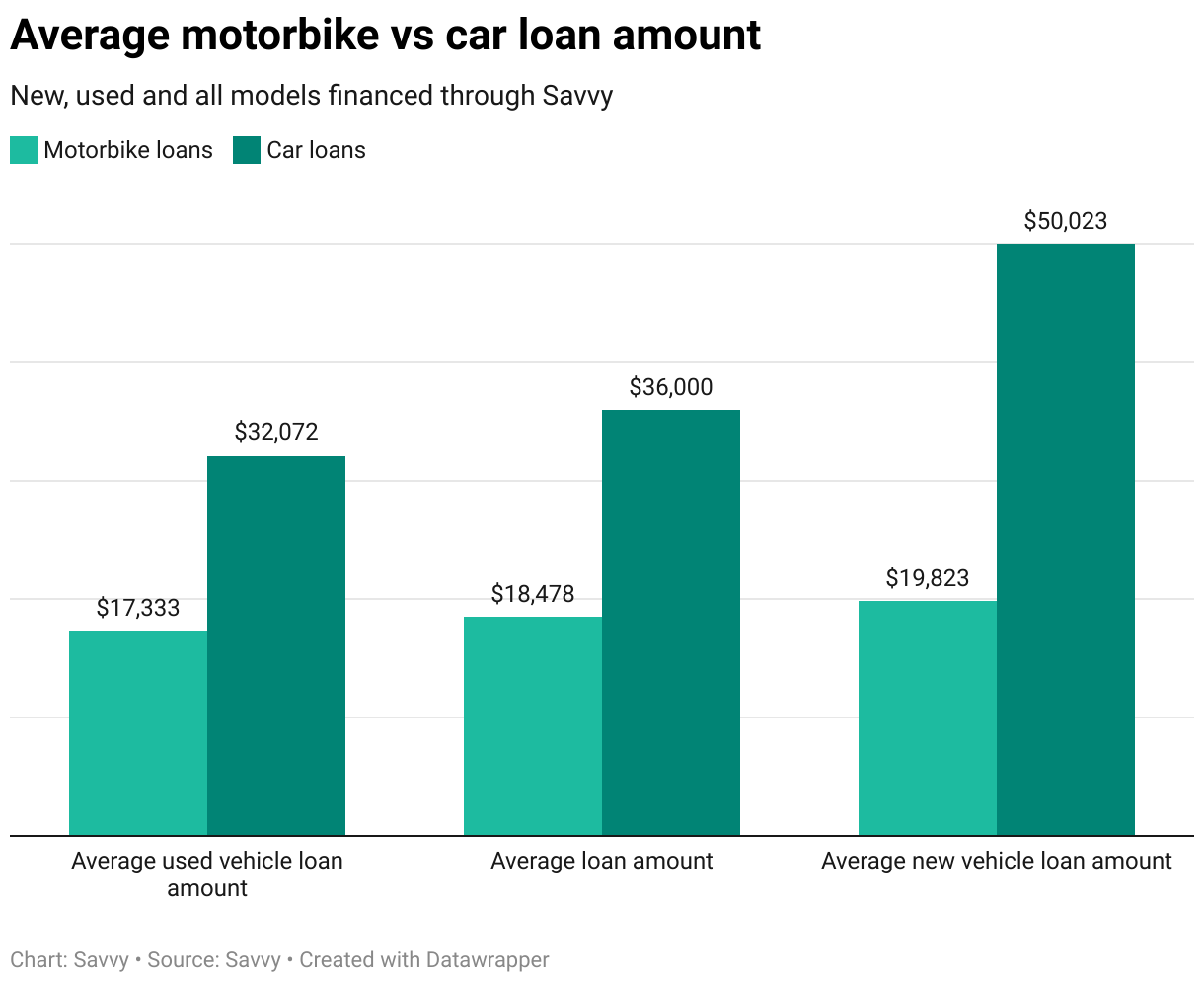

Using a calculator is a great way to approximate the cost of your loan before you apply, allowing you to work out what sort of loan you can afford that aligns with your budget. Even a small difference in interest rate, loan size or loan term will impact how much you’ll pay overall. The following examples show how much of a difference the purchase price and interest rate makes to the overall cost when buying a new or used model:

The cost of financing your motorbike: new vs used

Yamaha MT-07 LAMS

| Year | Price | Interest rate | Monthly repayment | Overall interest |

|---|---|---|---|---|

| 2022 | $12,000 | 11.36% p.a. | $263 | $3,784 |

| 2025 | $14,999 | 10.50% p.a. | $322 | $4,344 |

|

2022 2025 |

|

$12,000 $14,999 |

|

11.36% p.a. 10.50% p.a. |

|

$263 $322 |

|

$3,784 $4,344 |

Kawasaki Z900RS SE

| Year | Price | Interest rate | Monthly repayment | Overall interest |

|---|---|---|---|---|

| 2022 | $18,990 | 11.36% p.a. | $416 | $5,988 |

| 2025 | $21,910 | 10.50% p.a. | $471 | $6,346 |

|

2022 2025 |

|

$18,990 $21,910 |

|

11.36% p.a. 10.50% p.a. |

|

$416 $471 |

|

$5,988 $6,346 |

Harley-Davidson Low Rider S 117

| Year | Price | Interest rate | Monthly repayment | Overall interest |

|---|---|---|---|---|

| 2022 | $25,990 | 11.36% p.a. | $570 | $8,196 |

| 2025 | $35,990 | 10.50% p.a. | $774 | $10,424 |

|

2022 2025 |

|

$25,990 $35,990 |

|

11.36% p.a. 10.50% p.a. |

|

$570 $774 |

|

$8,196 $10,424 |

Prices for listed new and used models sourced in August 2025 from bikesales. Interest rates based on average new and three-year-old used motorbike loan rates approved for good credit applicants through Savvy in the 2025 calendar year. Calculations based on a five-year loan term and do not include other purchase costs such as loan fees, boat registration and more.

Even with a relatively small loan, you can see that an increased interest rate impacts your repayments. For instance, on the Yamaha MT-07 LAMS, you’d only end up paying just under $60 extra per month and $360 extra over five years by opting for the model that costs $3,000 more.

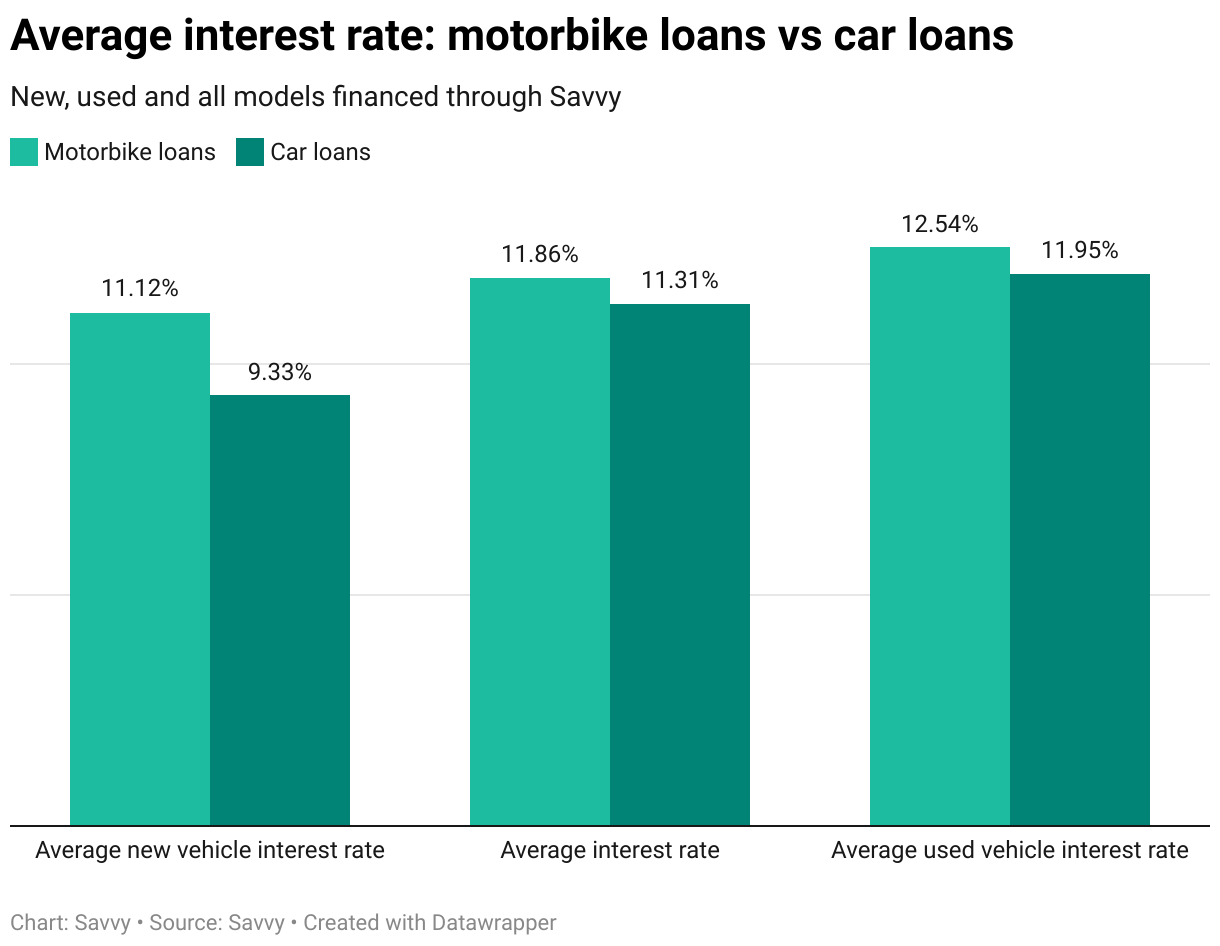

Why motorbike finance is more expensive than car loans

One thing you might’ve noticed is that the interest rates for motorcycle loans are a bit higher on average than car loans. Although each lender is different, the key area that they’ll be concerned about when it comes to financing a motorbike is safety.

According to the Department of Infrastructure, Transport, Regional Development, Communications and the Arts, motorcycle riders and passengers made up 21% of all road fatalities in Australia in 2024. 94% of these deaths were men.

On top of the risk to the driver, the severity of these accidents and the impact they have on the bike itself is often greater. As a result, motorbikes are more likely to be written off in an accident than a car.

Am I eligible for motorbike finance?

Each lender is different, but the eligibility criteria you’ll generally need to meet are as follows:

- You must be at least 18 years of age

- You must be an Australian citizen or permanent resident (or, in some cases, an eligible visa holder)

- You must be earning a stable income which is enough to comfortably support your repayments (this can start from as little as $20,000 to $26,000 per year)

- You must be employed and earning a consistent income from your job

- You must meet your lender’s requirements related to your credit score

- Your motorbike must meet your lender’s requirements related to type, age and condition

What documents will I need to apply for motorbike finance?

The documents you’ll need when you apply for a motorcycle loan with Savvy are:

- Front and back of your driver's licence (or another form of government-issued ID)

- Your last two consecutive payslips (or your last tax return if you're self-employed)

- Your Savvy application, consent form and credit guide (supplied by your consultant)

- Information about your motorbike, such as its model and age, is handy to have

- 90 days of bank statements may be requested, but not always

Financing your motorbike before you get your licence

"If you plan to purchase a motorbike, but don’t have your learner’s permit (Ls) yet, you will likely need to take out an unsecured loan like you would with a dirt bike."